Lumber & Wood Production

Lumber & Wood Production

Exploring the Lumber & Wood Industry

I’m back with another post about the Basic Materials Industry. This time it’s about Lumber & Wood Production. There are eight companies with a market cap over $1 Billion in the Lumber & Wood Production industry. We’ll cover those names but, first, let’s take a look at how construction wood is made:

Three of the seven names are headquartered in the United States. Those are UFP Industries, a provider of lumber to the manufactured housing industry, and Simpson Manufacturing, a manufacturer of wood construction products, including connectors, truss plates, and fastening systems, and the largest forest products company in the group, Weyerhaeuser Co.

Four of the remaining five companies in this space are headquartered in Canada. And the second largest of the group, Svenska Cellulosa, is headquartered in Sweden.

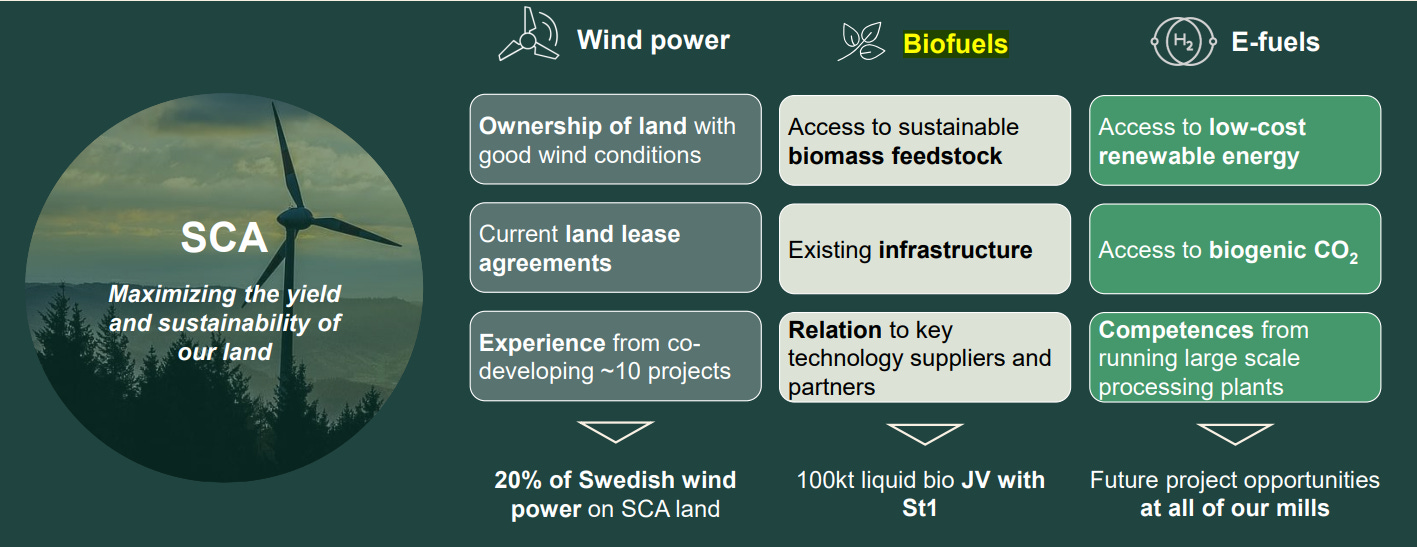

Svenska Cellulosa AB is Europe's largest private forest owner, with 2.7 million hectares of land in northern Sweden and the Baltic region. They own 6% of Sweden! Reportable segments (% of net sales Q4 2023) are Forest (28.96%), Wood (18.36%), Containerboard (21.20%), Renewable Energy (8.02%), Pulp (23.47%), and Logistics. They operate five sawmills, two pulp mills, and two Kraftliner mills. Two additional facilities are engaged in pellet production.

SCA’s Pulp segment encompasses the production and sale of bleached softwood kraft pulp (NBSK) and chemi-thermomechanical pulp (CTMP), produced at the Ostrand pulp mill, The Containerboard segment includes packaging paper with kraft liner manufacturing at the Obbola and Munksund paper mills, and The Renewable Energy segment which encompasses production and sales of processed and unprocessed biofuels as well as liquid biofuels. The company also leases out land for wind power.

With over 60 manufacturing facilities in the US, Canada, and Europe, West Fraser is the world’s largest lumber producer in the world. They manufacture building materials, including framing lumber, roof and wall sheathing, specialty OSB, trusses, flanges, flooring, rim boards, and door and garage door headers. West Fraser serves thousands of delivery points and customers across North America; the majority of product shipments use rail to transport Canadian SPF and OSB to U.S. markets and trucks to transport SYP and OSB from mills in the U.S. south.

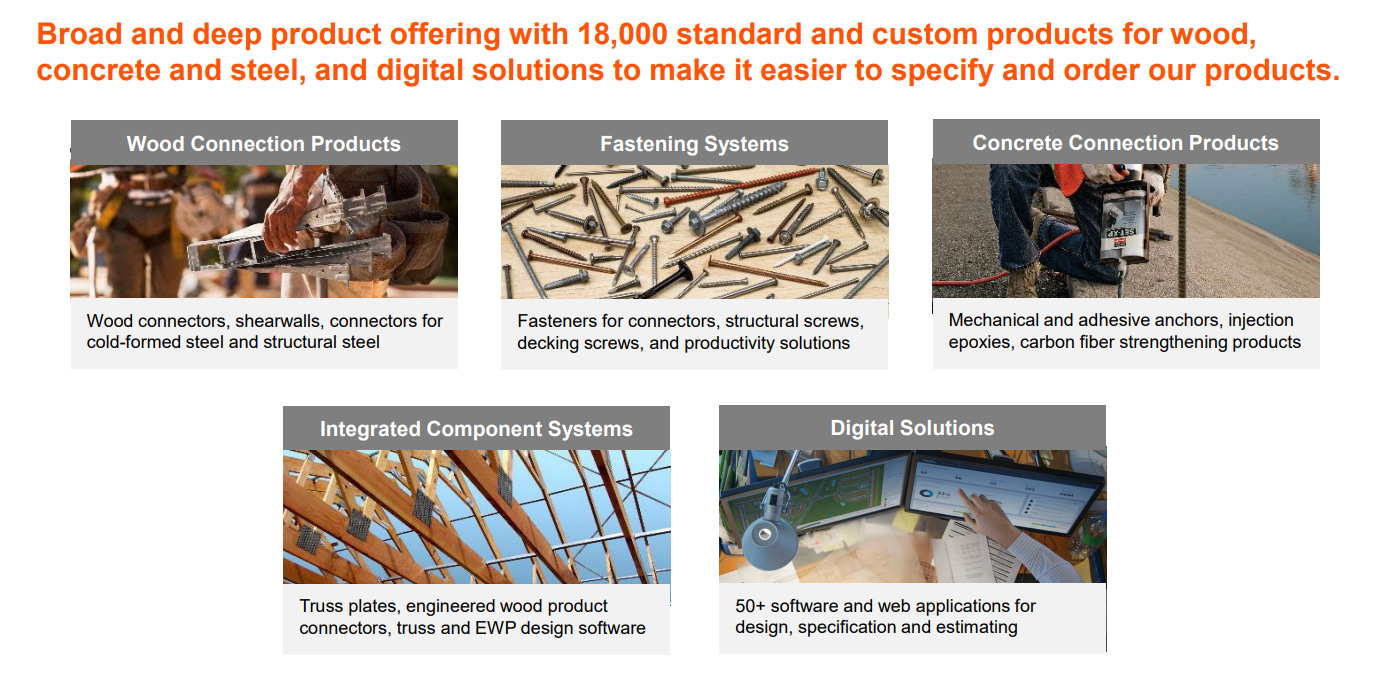

Simpson Manufacturing Co Inc manufactures and sells building materials, including connectors, truss plates, fastening systems, fasteners, prefabricated lateral systems, concrete construction products, adhesives, mechanical anchors, carbide drill bits, powder-actuated tools, and fiber-reinforced materials. The company markets its products to the light industrial, residential, and commercial construction markets as well as the remodeling and DIY markets. The Company is organized into three reporting segments defined by the regions namely North America, Europe, and Asia Pacific. The company generates the majority of its revenue (85% in 2023) from wood construction products sold in the United States. Concrete construction accounts for the other 15% of net sales.

With 219 facilities worldwide, UFP serves three markets: UFP Construction, UFP Retail Solutions, and UFP Industrial (packaging).

UFP Construction offers the complete package, from concrete to structure to finishes, as well as services such as design, transportation and installation.

UFP Retail Solutions include treated lumber through its ProWood brand, siding, shiplap, trim, and composite decking through its Deckorator brand.

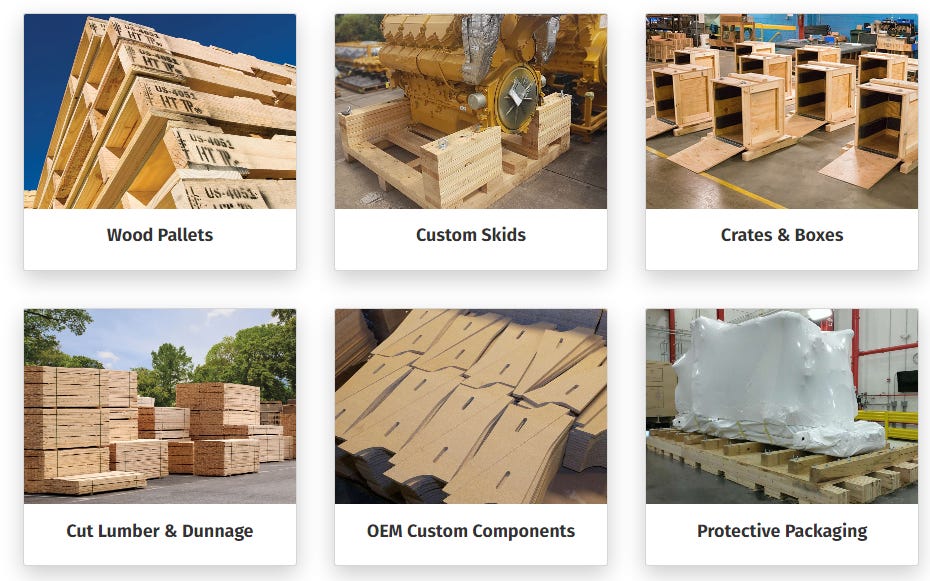

Through its Industrial segment, UFP manufactures and sells packaging solutions, including wood pallets, skids, crates and boxes, lumber & dunnage, cardboard, labels and label applicators.

Headquartered in Quebec, Stella-Jones is a leading North American producer of pressure-treated wood products. It supplies the continent’s major electrical utilities and telecommunication companies with wood utility poles and North America’s short line and commercial railroad operators with railway ties and timbers. Stella-Jones also provides industrial products and manufactures and distributes premium treated residential lumber and accessories.

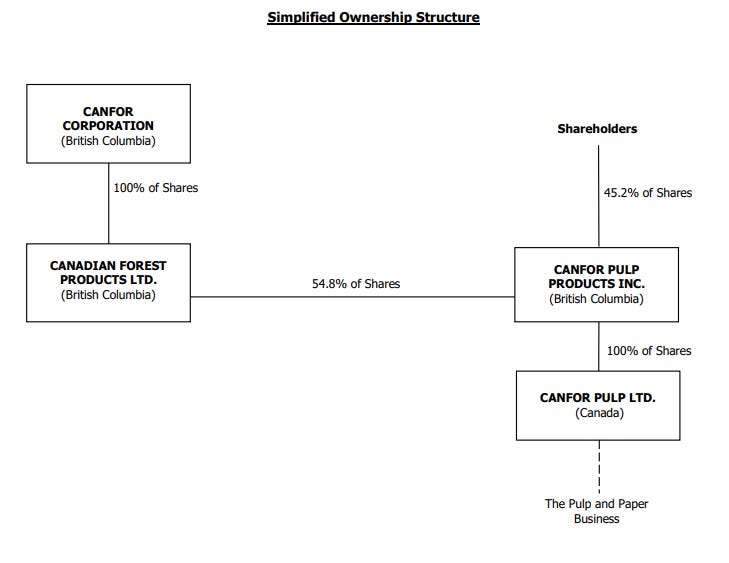

Canfor is a softwood lumber company that also owns around half of Canfor Pulp. It is active throughout North America and Europe, with lumber mills in British Columbia, Alberta, the Southeastern United States, and Sweden. It has two reportable segments: lumber and pulp and paper. The lumber segment includes Canfor's sawmilling and remanufacturing operations and the pulp and paper segment includes the kraft pulp, kraft paper, and bleached chemi-thermomechanical pulp businesses of Canfor Pulp. Pulp accounts for 77% of sales in the pulp and paper segment.

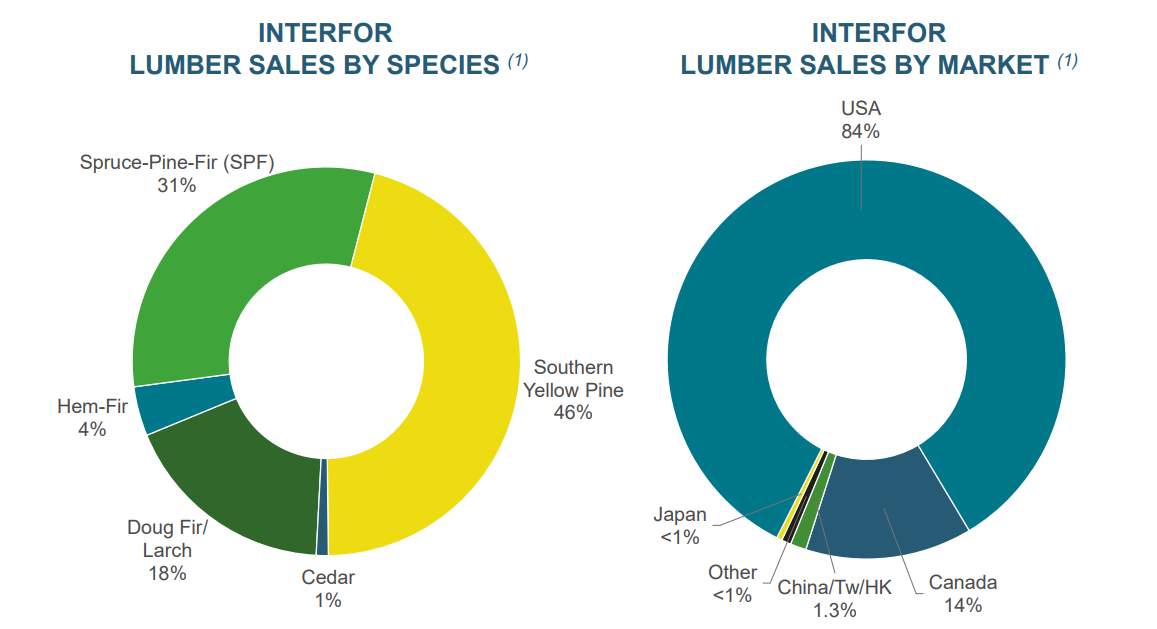

Interfor is one of the top three softwood lumber producers in North America, with 32 strategically located facilities and high exposure to US South, Eastern Canada and Atlantic Canada. Sales in the United States make up 84% of total sales, and

Weyerhaeuser ranks among the world's largest forest product companies. With 10.5 million acres held in the US & 14 million acres licensed in Canada, they’re the largest private owner of timberlands in North America. Following the 2016 sale of its pulp business to International Paper, Weyerhaeuser operates three business segments: timberlands, wood products, and real estate. Weyerhaeuser is structured as a real estate investment trust and is not required to pay federal income taxes on earnings generated by timber harvest activities. Earnings from its wood products segment are subject to federal income tax.

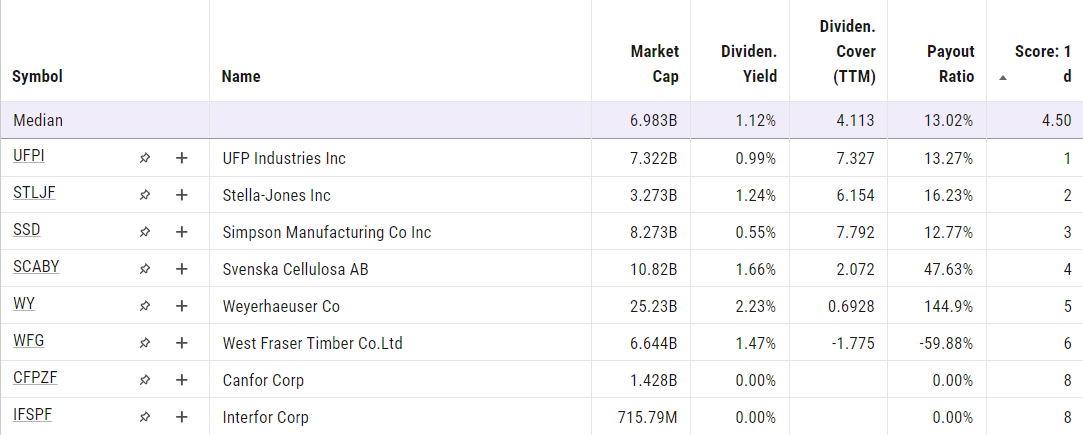

The median 10-Year Profit Margin for this group is 8.64%

Swedish Svenska Cellulosa wins out on Profit Margin.

UFPI takes the top spot with regard to FCF-to-Debt; however, that 2.815 FCF-to-Debt is offset by the slimmest margins in the group.

Svenska Cellulosa is investing the most of its retained earnings back into its business for long term operational growth. For every dollar it makes in revenue, it’s spending 17 cents on capital expenditures meant to expand revenue-generating capabilities.

At 2.23%, Weyerhaeuser has the highest dividend in the group. But its 0.6928 cover & 144.9% payout isn’t attractive. Using a 34-33-33 (yield, cover, payout) ranking model, UFPI’s relatively small 0.99% dividend yield is the winner. This is due to it being able to pay that 0.99% 7.3 times over, if need be. Dividend health > dividend yield.

d-dividend

f-fcf-to-debt

p-10y Profit Margin

ce-capex-to-revenue

a- combined, equal weight

Books Ranked as of today, 4/7/2024.

SCABY

SSD

WY

UFPI

STLJF

WFG

CFPZF

IFSPF